Many people ask the same questions: “Is now a good time to get into the market?” or “Should I sell everything and get out for a while?” These questions seem sensible, but they’re based on a huge misunderstanding.

The truth is, you can’t really “get out” of the market. From the moment you earned your first dollar, you became an investor. You’ve been playing the game all along, whether you realized it or not.

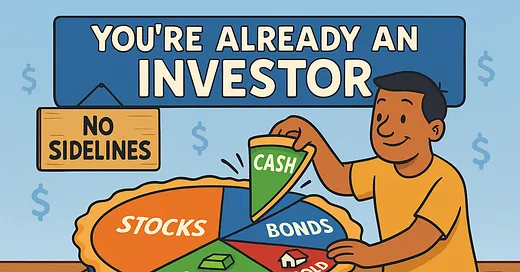

The only real question is how you are investing.

1. There Are No “Sidelines”—Only Different Places to Put Your Money

Forget the idea of “entering” the market when you buy a stock and “exiting” when you sell. Think of all your money as being part of one big personal pie. Every dollar you have is a slice of that pie, and every slice has to be placed somewhere.

This is called your asset allocation. It’s simply the mix of different things you own. Your choices include:

- Cash in a Bank Account: You might think of this as being “on the sidelines.” But it’s not. Keeping money in a savings or checking account is an investment choice. You are choosing to prioritize perfect safety and immediate access above all else. The trade-off? Your money earns very little and actually loses buying power over time due to inflation (the slow rise in the price of everything). Your cash is an investment in stability, but it’s a “leaky bucket” that slowly loses value.

- Stocks (or Equities): This is owning small pieces of actual businesses (like Apple, Target, or your local power company). This is an investment choice you make for growth. You’re betting that these companies will innovate, grow, and become more valuable over the long term.

- Bonds: This is like lending your money to a government or a company. In return, they promise to pay you back with interest. This is an investment choice you make for income and relative stability. It’s often a middle ground between the safety of cash and the growth potential of stocks.

- Real Estate, Gold, etc.: Owning your home or other assets are also investment choices, each with its own reasons and risks.

Do you see the pattern? Your money is never doing “nothing.” It’s always allocated somewhere. You aren’t deciding whether to invest; you are constantly deciding how your money is invested. The game doesn’t start when you call a broker; it started the moment you got paid.

2. Why the Slices of Your Pie Matter So Much

Over a lifetime, how you slice your financial pie has life-changing consequences. This is because of the power of compounding, where your returns start earning their own returns.

Let’s revisit that incredible math:

- If you choose slices that give you a 3% annual return after inflation (typical of a very “safe,” cash-heavy pie), $1 grows to about $4.40 over 50 years.

- If you choose slices that give you an 8% annual return (more typical of a pie with a large slice of stocks), that same $1 mushrooms into roughly $47.

That staggering difference comes from dedicating a meaningful slice of your pie to a growth engine. For most people, throughout history, that growth engine has been stocks. Why? Because you are owning a piece of productive businesses that are designed to grow.

Of course, the “growth slice” of your pie is also the bumpiest. Its value will go up and down (this is volatility). But panicking and selling this slice during a downturn is like jumping out of a powerful car just because the road got a little rough.

3. Adjusting Your Slices, Not “Exiting the Game”

So, if you’re always invested, how should you think about making changes? You don’t “exit”; you simply reallocate. You change the proportions of your pie slices.

Here’s a practical way to think about it:

- The “I Need It Soon” Slice (Cash & Equivalents): Everyone needs a slice dedicated to near-term needs (about two years of living expenses). This is your safety buffer. It’s the money for a leaky roof or a sudden car repair. You keep this in ultra-safe places like a high-yield savings account or a money-market fund so you never have to sell your long-term investments at a bad time.

- The “Sleep Well at Night” Slice (Your Comfort Level): If seeing your investments drop makes you deeply anxious, your “Safety” slice might need to be bigger. That is perfectly fine. The goal is to create a pie you can live with. Just understand the trade-off: a larger safety slice means a smaller growth slice, likely leading to a smaller pie in the very distant future.

- Rebalancing Your Pie: Let’s say you own stock in Microsoft. After a great year, you notice the Microsoft slice has gotten much, much bigger, while your cash slice looks small. You might feel your pie is off-balance and riskier than you’dlike.Youdon’t think, “I need to get out of the market!” Instead, you think, “I’m going to rebalance my pie.” You might sell a small portion of your Microsoft stock and add the money to your cash or bondslice.Youhaven’t “exited.” You’ve simply trimmed one slice and beefed up another to bring your personal pie back to a mix that feels right for you. It’s like rotating the tires on your car for a smoother long-term ride, not abandoning the car on the side of the road.

Coming Up Next: How to Allocate Your Money and Why the Stock Market Is a Better Place

We’ve established the most important rule: you are always an investor, and your main job is to decide how to slice your financial pie.

This naturally leads to the two most important questions of all:

- How, exactly, should a beginner allocate their money? What should the slices of the pie look like?

- We know stocks have a history of growth, but what makes the stock market such a powerful place for building wealth over the long run compared to other options?

Answering these questions is the key to turning this knowledge into a real, actionable plan for your future.

I will break down the answers in detail in my next post. Stay tuned.

Relax to Rich — Calm, Thoughtful Investing

Pingback: Slicing the Pie: A Practical Guide to Investing Your Dollars for the Long Haul - Relax to Rich Club